What is Share

Meaning of Share

Share in the financial market refers to the small unit of ownership of a company. In other words, a share refers to the percentage of ownership in a company’s financial assets. The investor who holds at least one share in a company is known as a shareholder. This investor can be a person, institution, or a company.

Types of Shares

1. Equity Shares

Equity shares refer to those shares the amount of which is returned to the shareholders if the company’s all assets get liquidated and its debt is paid off at the time of winding up of the company. These shares are mentioned under the Equity and Liability head of the Balance Sheet. Most of the equity shares provide voting rights to the shareholders. There is not any fixed rate of dividend provided by these shares and the company can also skip to pay the dividend if profit in a particular year is not sufficient.

These shares are further divided into the following types:

- Bonus Shares

- Rights Shares

- Sweat Equity Shares

- Non-voting Shares

- Dividend Shares

- Growth Shares

- Value Shares

2. Preference Shares

Preference shares are those shares the dividend on which is paid before paying the dividend to the equity shareholders. In the case of bankruptcy or the winding up of the company, the payment is made to these shareholders from the company’s assets prior to equity shareholders. Most of these shares have a fixed rate of dividend and the company is bound to pay it every year. However, preference shares do not offer any voting right to the shareholder.

Preference shares are further divided into the following types:

- Cumulative Preference Shares

- Non-cumulative Preference Shares

- Participating Preference Shares

- Non-participating Preference Shares

- Redeemable Preference Shares

- Irredeemable Preference Shares

- Convertible Preference Shares

- Non-convertible Preference Shares

Valuation of Shares

The process of knowing the real value of the company’s shares refers to the valuation of shares. The value of shares can fluctuate with the market forces of demand and supply. It is easy to know the share price of a listed company but with private companies, it is an important and challenging task. This valuation is done by using various quantitative techniques which include the following three methods:

1. Asset-based Method

Under this approach, share valuation is done by calculating the value of intangible assets and contingent liabilities. This approach is highly useful for manufacturers, distributors, etc. who use a large value of capital assets. The formula used under the asset-based method is as follows:

Value per Share = (Net Asset – Preference Share Capital) / (Total Number of Equity Shares)

2. Income-based Method

When the valuation is done for a small number of shares, then this method can be useful. Here, the focus is on the income earned by the business from its investments, i.e., the profit generated by the business in the future. This approach can be further divided into two parts: Discounted Cash Flow (DCF) and Price Earning Capacity (PEC). The formula for the share valuation under the income-based approach is as follows:

Value per Share = Capitalized Value / Total Number of Shares

3. Market-based Method

Under this method, the share prices of the comparable public traded companies and the asset or stock sales of comparable private companies are used to calculate the value per share. The companies can easily collect the data of private companies from various proprietary databases but the main task is to choose comparable companies.

Who is a Shareholder?

Any person, company, or institution that holds or owns at least one share of a company’s stock, is known as a shareholder in the company. Shareholders enjoy the benefits from the company’s success in the form of increased stock valuation or dividends (profit distributed by the company to its shareholders). Conversely, when a company suffers a loss, the prices of the shares may drop invariably which can cause a decline in the value of the shares and also in the portfolios of the shareholders.

As per their stake in the company, the shareholders can be of two types: majority shareholders (those who hold majority shares in the company’s stock, i.e., more than 50%) and minority shareholders (those who holds minority shares in the company’s stock, i.e., less than 50%).

Other than this, the shareholders can also be divided as per the types of shares they hold in the company. Those who hold the equity shares and have the voting right in the company’s general meeting are known as common shareholders. While those who hold the preference shares and do not have the voting right are known as preferred shareholders. But, these shareholders have priority over the company’s profit that is distributed in the form of dividends.

Terminology

- Shares Outstanding

All the shares that have been authorized, issued, and purchased by the investors and are held by them, are known as shares outstanding. They include both the shares blocks held by institutional investors and the restricted shares owned by the company’s officers and insiders. These shares are presented under the heading “Capital Stock” of the company’s balance sheet. - Treasury Shares

Previously outstanding shares that are bought back from the shareholders by the issuing company are known as treasury shares. These shares are also called reacquired shares. Buyback of these shares causes a decrease in the total number of outstanding shares in the open market. Treasury shares are not part of the distributed dividends or the calculated earnings per share (EPS). Treasury stocks are calculated by using two methods: Cost Method and Par Value Method. - Shares Authorized

The maximum number of shares that a company is legally permitted to issue to the investors as specified in the article of association is known as shares authorized. Authorized shares are mentioned in the capital section of the company’s balance sheet. The number of these shares can be increased by the shareholders at the annual shareholder meetings but only if the majority of the shareholders are in the favor of the change. - Issued Shares

The shares that are issued by the owner in the share market or can say that the owner of the corporate wants to sell in the exchange of cash are known as issued shares. The number of shares issued by the company can be less than the number of shares authorized or demanded by the investors. When a company creates newly issued shares then it is called issuance, allocation, or allotment.

Tax Treatment of Dividends

Tax treatment of dividends varies between tax jurisdictions. In India, there is no tax charged on dividends in hands of shareholders up to INR 1 million. But the company which is using dividends has to pay dividends distribution tax at the rate of 12.5 percent. In our country, there is also the concept of a deemed dividend that is not tax-free. Further, the tax laws of the country include provisions to stop dividend stripping.

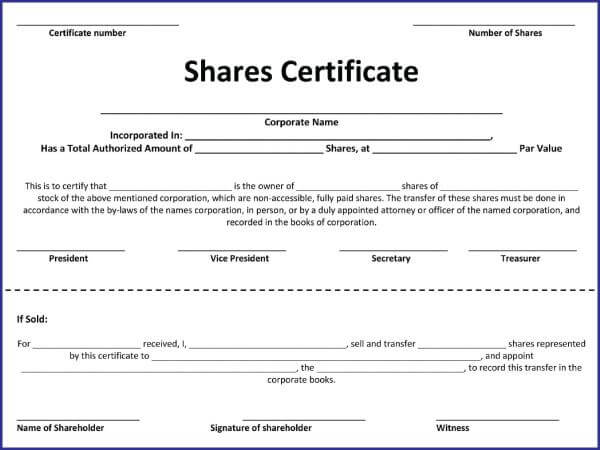

What is Share Certificate?

Prior to the introduction of the Demat account and digital shares, a share certificate was issued to the investors as proof of their ownership in the company’s shares. Now the concept of share certificates has been replaced with digital certificates. The ownership of the shareholders is recorded in electronic form by a system such as CREST or DTCC, a central securities depository.

Difference between Shares and Stocks

| Comparison of Basis | Shares | Stocks |

|---|---|---|

| 1. Meaning | Share refers to the smallest part of the company’s share capital which represents the shareholder’s ownership in the company. | Stock refers to the bundle of shares that are owned by a member of the company. |

| 2. Denomination | Investors can buy multiple shares of a company that has equal value. | Investors can buy the stocks of a company having different types and different values. |

| 3. Possibilities of Original Issues | Shares are always issued originally. | Stocks can’t be issued originally. |

| 4. Nominal Value | They have nominal value. | They don’t have nominal values. |

| 5. Numeric Value | A share has a specific numeric value that is related to a specific company. | Stocks do not have a numeric value and can be related to one or more companies. |

| 6. Paid-up Value | They can be partly as well as fully-paid. | They are always fully paid. |

| 7. Transfer | Shares can be transferred but not into the fractions. | Stocks can be separated into any amount and thus can be transferred into fractions. |